This a re-post of an article written in October 2009 following Atul Gawande‘s article in the New Yorker on the ‘cost conundrum‘ which launched his presence and eventual celebrity on the national stage. Gawande was calling attention to the regional variations (small area analysis) in the Medicare spend and associated health disparities that can be found in the United States while generally adjusting for comparable characteristics of each community. The comparison of Medicare costs in El Paso vs. McAllen caught and retained my attention as many years later the discrepancy remains largely unresolved.

One might ask why?

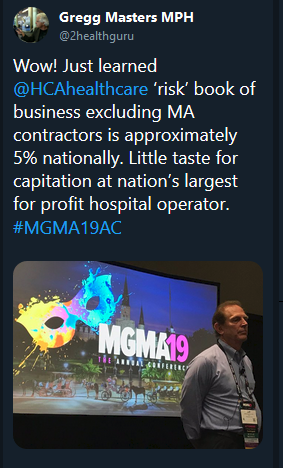

Having just returned from the Medical Group Management Association’s (MGMA) annual conference in New Orleans, I was struck by and tweeted out the following observation reported by the largest for-profit hospital operator in the U.S.:

Some 10 years later this 5% ‘share’ of risk  business is evidence that the healthcare landscape (at least at the hospital or health system level and especially so for the for-profit sector) remains a risk averse, “heads in beds“, fee for services economy with pockets of innovation demonstrating value, while for the remainder of the cohort there’s little appetite for risk assumption beyond toe in the water shared savings or bundled payment commitments.

business is evidence that the healthcare landscape (at least at the hospital or health system level and especially so for the for-profit sector) remains a risk averse, “heads in beds“, fee for services economy with pockets of innovation demonstrating value, while for the remainder of the cohort there’s little appetite for risk assumption beyond toe in the water shared savings or bundled payment commitments.

Unfortunately, ‘value based healthcare‘ often a proxy for capitation (full or partial), all in population based payments or downside risk assumption remains mostly ‘ad copy‘.

For more information on the dubious claims of health system horizontal and select vertical mergers, listen to ‘BS in Healthcare‘ interview with Layton R. Burns, PhD, Professor and Director, Wharton Center for Health Management and Economics, at the Wharton School.

In the aftermath of Atul Gawande’s landmark piece ‘The Cost Conundrum‘ and the selective emergence of the ‘Mayo v. McAllen‘ mantra, I’ve been tweeting of late on the ‘irony’ of certain Texas health markets, particularly given the concentration of hospital assets in non profit health systems, and the timely question of whether such consolidations produce the ‘community benefits’ proffered by their leadership. The recently published Commonwealth Fund study ‘Aiming Higher: Results from a State Scorecard on Health System Performance, 2009‘ has supplied certain metrics to further contextualize the conversation.

First some background: I spent 13 years in the Lone Star state, initially advising a major national proprietary hospital management company’s implementation of its managed care strategy in the Houston market, followed by implementation physician networks for a 140,000 member global risk Medical Group, and finally managing payor and provider contracts for a joint venture ‘Super PHO’ affiliated with a dominant faith based hospital system in Dallas/Fort Worth.

Now mind you, everything in Texas is big – especially its delivery system players who have literally architected quite beautiful (and very expensive) ’cathedrals of medicine’. Examples include: the Texas Medical Center (an NIH like cluster of some 12+ competing institutions), Memorial Hermann Health System, Baylor Health Care System and Texas Health Resources to name a few of the trophy properties. Yet, years after the roll out of the strategic plans of these health systems, and the fulfillment of their market share objectives, certain of the state’s health care indicators look quite grim when contrasted to other parts of the country.

One might wonder why? Afterall, the typical pre-merger or alliance argument in favor of consolidation, acquisition or market expansion, was typically framed as follows, it will:

- Improve quality

- Improve access

- Increase operating efficiencies; and

- Lower costs

Yet according to the Commonwealth Fund study, and now years after these consolidations, here’s how Texas ranks on key metrics of health status compared to all 50 states, and the District of Columbia.

- Overall: 46

- Access to care: 51

- Prevention & Treatment: 43

- Avoidable Hospital Use & Costs: 42

- Equality between rich and poor: 50

- Equality between non-Hispanic white and minority: 48

- Healthy lives: 21

- Children with medical and dental check-ups in past year: 40

- Adults with a regular doctor: 49

- Medicare reimbursements: 46

- Infant mortality: 19

- Breast-cancer deaths: 18

- Colorectal cancer deaths: 15

- Adults who smoke: 17

- Overweight or obese children: 32

Not exactly ‘best in class’. So why not ask, where is the ostensible and promised ‘community benefits’ and not just those codified in IRS code, to justify the tax exempt status for most of the entities above? How is this ‘return’ (to the community) being measured; (is it via Medicare or Medicaid ‘shortfalls‘, or charity and bad debt write-offs; or some tangible real world contribution); or is it even accurately measured? The IRS 990 filings are somewhat ‘fluid’ on the specific reporting of activities that count towards community benefit.

Most, if not all, of these institutions are primarily ‘non profit’ (with some affiliate JV exceptions) yet they are aggressively managed to generate a surplus of revenue over expenses; after all ‘no margin, no mission’. While they do not have stock holders or investors per se, they do have bonds that require adequate debt service coverage in order to maintain favorable credit ratings and competitive access to capital.

This is where the ’story’ for the consolidations and, for some, the unspoken truth of the matter emerge, IMO. While perhaps stated in the vision for some, most of the benefits of consolidation are to be found in the pricing leverage that comes from asset concentration. Hospitals want higher rates, and payors (health plans and insurance companies) can tell you how difficult it was, and likely remains today, to extract material discounts from these massive institutions given their scale and market dominance.

So the question remains open: have they delivered, or are they just plain ‘doin’ it wrong’? Is the promised value proposition a reality today for the Texas residents they purport to serve? Based on these, and other metrics, many would say no. Rather than more of these Texas sized giants, why not refocus the Lone Star state on their one home grown version of a ‘Mayo Clinic’ model domiciled in Temple, Texas aka ‘Scott and White‘.

In the next blog post, i’ll touch on the physician role in the Texas market, and the historical rise and fall of physician driven integrated delivery systems in particular.

==##==