Editor’s Note: This is the first in a series of posts on ‘Patient Safety’ and specifically the NMP (“not my patient, not my problem”) problem in medicine.

I recently participated in the World Patient Safety Dayin Washington, D.C., September 17th, 2024, with organizing founding members of the Patients for Patient Safety, U.S., an affiliate of WHO (World Health Organization). We marched, then gathered for a ‘remembrance ceremony‘ for those lost, harmed or disabled due to medical error(s).

Anthony John Masters

The event is introduced by Martin J Hatlie, JD, President & CEO, Project Patient Care for Patients for Patient Safety Day D.C.:

The first post sets context for the series framing the nature of the problem and range of suggested solutions. Additional context for the series can be found at EndNMP.org

In 2016, a controversial study published in the British Medical Journal (BMJ) “Medical error—the third leading cause of death in the US” suggested that medical errors were the third leading cause of death in the United States, claiming over 250,000 lives annually. This statistic sent shockwaves through the medical community and sparked intense debate about both the accuracy of the number and the methodologies used to arrive at such estimates. Seven years later, we’re still grappling with the fundamental question: How many Americans actually die from medical errors each year?

The Current Landscape

Truth be told, we don’t know the exact number of deaths attributable to medical error(s) – and that’s part of the problem. Current estimates vary widely, ranging from 22,000 to over 440,000 (and above) deaths annually, reflecting the significant challenges in measurement and classification. The Centers for Disease Control and Prevention (CDC) doesn’t require reporting of medical errors on death certificates, and there’s no standardized methodology for capturing this data.

Why Such Wide Variations?

Several factors contribute to the dramatic range in estimates:

1. Definition Discrepancies: There’s no universal definitionof what constitutes a medical error. Some studies include only clear mistakes, while others encompass broader categories of preventable harm.

2. Reporting Mechanisms: Death certificates, the primary source for mortality statistics, don’t have a standardized way to indicate medical error as a cause of death.

3. Detection Challenges: Many errors go unnoticed or are not documented due to fear of litigation or professional repercussions.

Current Methodologies and Their Limitations

1. Global Trigger Tool (GTT) – Is a methodology developed by the Institute for Healthcare Improvement (IHI) to identify adverse events in medical records. It uses “triggers” (or clues) to identify possible adverse events, which are then investigated further to determine if an actual adverse event occurred.

Pros:

– Systematic approach using specific criteria

– Can identify errors that might otherwise go unnoticed

Cons:

– Labor-intensive and time-consuming

– Subject to reviewer interpretation

– May not capture all types of errors

2. Voluntary Reporting Systems

Pros:

– Can provide detailed information about specific incidents

– Helps identify patterns and systemic issues

Cons:

– Severe underreporting due to voluntary nature

– Bias towards more obvious or serious errors

3. Retrospective Chart Review

Pros:

– Comprehensive examination of patient records

– Can identify patterns and contributing factors

Cons:

– Time-consuming and expensive

– Subject to hindsight bias

– Limited by quality of documentation

The Case for Accurate Measurement

Despite definitional, measurement and reporting challenges, there are compelling reasons to pursue more accurate measurement of deaths from medical errors:

1. Patient Safety Improvement: Accurate data can help identify patterns and systemic issues, leading to targeted interventions and improved safety protocols.

2. Resource Allocation: Better data can inform where to focus quality improvement efforts and resources.

3. Accountability: Accurate measurement can drive accountability and motivate healthcare organizations to prioritize safety.

The Counterargument

Some argue that focusing too heavily on exact numbers could be counterproductive:

1. Defensive Medicine: Fear of being labeled as ‘error-prone‘ might lead to overly cautious medical practices and only reinforce what some referred to as the ‘blue wall of silence’, ie,, ‘thou shall not speak ill of one’s peers’.

2. Morale Impact: Constant focus on errors could demoralize healthcare workers and impact recruitment. ‘Clinical burnout‘ is already an epidemic for our often over worked and under supported clinicians.

3. Resource Diversion: Time and resources spent on measurement might be better used for direct patient care improvements and learnings from review of suboptimal outcomes, care gaps or poor handoffs during shift changes, etc.

Potential Solutions

Short-term Improvements

1. Standardized Definitions: Develop and implement consistent definitions of medical errors across healthcare systems.

2. Enhanced Reporting Systems: Create protected, anonymous reporting systems to encourage more accurate documentation.

3. Death Certificate Reform: Add specific fields for recording medical errors as contributing factors to death.

Long-term Strategies

1. AI and Machine Learning: Develop sophisticated algorithms to detect potential errors in real-time and analyze patterns across large datasets.

2. Culture Change: Foster an environment where error reporting is seen as a learning opportunity rather than a punitive measure.

3. National Database: Create a standardized, national system for recording and analyzing medical errors.

The Role of Technology

Emerging technologies offer promising solutions for more accurate measurement:

1. Natural Language Processing: Can analyze medical records to identify potential errors that human reviewers might miss.

2. Blockchain: Could provide secure, immutable records of medical events, making it easier to track and analyze errors.

3. Big Data Analytics: Can identify patterns and risk factors across large populations, potentially predicting and preventing errors before they occur.

Conclusion

While perfect measurement of deaths from medical errors may be an unrealistic goal, significant improvements are both possible and necessary. The path forward likely involves a combination of technological solutions, policy changes, and cultural shifts in the medical community.

As we work towards better measurement, we must balance the need for accuracy with the potential negative impacts of excessive focus on errors. The ultimate goal should be to create a healthcare system where errors are promptly identified, openly discussed, and systematically addressed – not to assign blame, but to save lives.

By taking a thoughtful, balanced approach to this challenge, we can work towards a healthcare system that is both more accountable and more effective at preventing harmful errors.

—

*Note to readers: This blog post aims to provide a balanced overview of a complex issue. The statistics and methodologies discussed are based on currently available research, but given the nature of the topic, exact numbers remain subject to debate and ongoing study.*

Whoa! Not 24 hours after the Request for Information (RFI) issued by WalMart Health and Wellness directed to it’s ‘strategic partner’ downline hit the street, I mean was leaked to the press, WalMart’s senior management felt compelled to promptly backdown from it’s rational, comprehensive, timely and sensible approach to make a meaningful dent into the US Healthcare, I mean, ‘Sickcare’ quagmire, by issuing the following terse statement:

Walmart Statement in Response to Health & Wellness Request for Information

“The RFI statement of intent is overwritten and incorrect. We are not building a national, integrated, low-cost primary care health care platform.”

– John Agwunobi M.D., Senior Vice President & President of Walmart U.S. Health & Wellness

Yikes! What’s behind this ‘whiplash’ effect?

It’s not news that WalMart has a mixed history with respect to the way they manage or evade (depending on your point of view) offering health benefits as an incentive to their less than full time staff. Yet, WalMart is the ‘400 pound gorilla’ as Chukwuma I. Onyeije, M.D., aka@chukwumaonyeije opined in a Google+ thread to a pool of health care social media peeps on Wednesday.

Regardless of the creative health benefits offer or ‘avoidance strategy’ for their part time staff, WalMart who’s gross sales account for approximately .5% of total US GDP, is a behemoth and perhaps second only to the Federal Government, the single largest ‘wholesale buyer’ of health benefits in the US.

So when they retained Price Waterhouse Coopers to consult on the compiling and distribution of an RFI to the tighly held ‘strategic partner’ network, they clearly intended to step into the population management fray of the payor/provider conundrum. You know, your costs are my revenues…

I’ve suspected all along, that while many on the provider side whine about CMS, the PPACA and now final rule to implement ACOs, many forward thinking peeps, mostly the Wall Street crowd who smell profits in those emerging re-engineered rules around population health management are stepping foward, perhaps aided and abetted by the so called ‘2nd in position skin in the game’ employer community.

We’ll watch and report with interest how this drama and retraction plays out.

How the Insurance Companies Took Over the HMO Industry & the Raid on FHP International

An Enhanced Reconstruction of the Robert Gumbiner MonographCross-referenced and augmented from oral history, SEC filings, corporate histories, and contemporaneous press sources

by Gregg Anthony Masters, MPH** Managing Director, Health Innovation Media | Executive Producer, Healthcare NOW Radio

Let me be direct: every policy conversation I’m having right now about ACOs, value-based care, and the so-called ‘transformation’ of American healthcare runs through a ghost – a Southern California physician who built something remarkable, watched it get strip-mined by a board and an investment banking culture that never understood what he’d built, and spent his final years putting the story on paper so we couldn’t pretend it didn’t happen.

His name was Robert Gumbiner, MD. His creation was FHP International Corporation. And his posthumously published monograph – The HMO, Taking It All Apart: The End of a Dream (AuthorHouse, 2009) is one of the most important and least-read documents in the history of American managed care.

I’ve been a soldier in this space long enough to have watched the managed competition experiment arc from insurgent idea to institutional furniture to convenient villain. I mainstreamed HMOs and second-generation PPOs in California back when the AMA still treated prepaid group practice like a communicable disease. So when I say Gumbiner’s story is our story – the story of everyone who has ever believed that organized, prevention-focused, physician-led care could actually work – I’m not being romantic. I’m being precise.

Before HMO Was a Dirty Word

Long Beach, California. 1961.

Gumbiner had already run the arc that defined his generation’s most serious physician-thinkers: Indiana University MD (1948), migration west, a stint as an Air Force physician during Korea, which exposed him to the logic of population-based capitated care and then a decade in private practice at Plaza Medical Group with nine other physicians, during which he’d been quietly running a prepaid plan for their patients. He understood, at an almost molecular level, what fee-for-service medicine was doing to the doctor-patient relationship: it rewarded illness, not health. He called it “basically immoral,” because it meant doctors earn the most when patients are sickest.

So in 1961, he converted Plaza Medical Group into a nonprofit corporation, Family Health Program, with 2,000 enrolled members prepaying a flat monthly fee for comprehensive care delivered by employed physicians under one roof. This is what we now call the staff-model HMO. At the time, it was barely tolerated by organized medicine and invisible to most health policy observers.

By the end of the 1950s, Gumbiner recalled in the Orange County Business Journal, “there were only a few dozen HMOs around the country.” When he launched, the concept had a lineage, i.e., Kaiser’s industrial prepaid plans from the 1930s, the Group Health Association in DC, but it was emphatically not mainstream. It was, in fact, exactly the kind of structural insurgency (in today’s parlance ‘innovation’) that establishment, legacy or mainstream medicine and insurance industry incumbents were designed to suppress.

What Gumbiner built over the next two decades is, by any honest accounting, one of the great organizational achievements in American healthcare history:

1967: 10,000 members. Second Long Beach center.

1968: Third center, Fountain Valley, Orange County.

1969: Medicaid pilot launched, one of the first HMOs in the country to serve low-income beneficiaries, at a time when most of the industry thought Medicaid was financial poison.

1971: 30,000 members at the ten-year mark. Compton center added.

1973: Guam. Which tells you everything about his ambition and his eccentricity.

1977: Federal HMO qualification, opening eligibility for Medicare and Medicaid reimbursement.

1982: Medicare risk contract pioneer – Family Health received a federal demonstration contract to provide prepaid capitated care to seniors, assuming full actuarial risk that the patient’s care might exceed the flat fee. This is the model that became Medicare Advantage. Gumbiner’s shop essentially invented it for the West Coast.

1983: FHP Senior Plan launched. The company converted a Long Beach skating rink into a Senior Health Plan Center to handle the flood of new elderly members.

I’ve thought about that gap for a long time. At the time, it looked like savvy maneuvering. In retrospect and this is the argument Gumbiner makes explicitly in his monograph and in the two-volume oral history he gave to UC Berkeley’s Bancroft Library in 1996, it was the opening through which a different set of institutional logics entered the organization. The IPO followed in July 1986 on NASDAQ. The board composition changed. Wall Street’s quarterly cadence became a structural fact of life. And the incentive architecture that had produced three decades of mission-driven growth began, slowly, to be reoriented around something else entirely – something I’ve referred to as the ‘HealthcareBorg‘ where all meaningful innovation goes to die via assimilation by the incumbents – which just might explain the hostility towards the entire for profit health insurance domain.

The IPA expansion accelerated during this period via more mainstream docs in Individual Practice Associations, networks of independent physicians contracted rather than employed. Faster to stand up than a new medical center, cheaper in capital terms, easierto scale across new geographies. Also, in Gumbiner’s view, a vector through which fee-for-service logic seeped back into what was supposed to be a capitated, prevention-focused enterprise. You cannot supervise the clinical behavior of 10,000 contracted independent physicians the way you can manage 200 employed ones. The model that made FHP FHP, i.e., an integrated, accountable, coherent ecosystem, began to diffuse.

In 1990, Gumbiner stepped back from day-to-day operations. The board was now running the company. Within months: a major malpractice jury award. A Medicare rate increase of only 1.4 percent. Federal scrutiny of FHP’s aggressive Medicare marketing in San Diego. The architecture was holding, but the foundation had shifted.

FHP at that moment served nearly 2 million HMO members in 11 states and Guam – commercial, governmental, and Medicare beneficiaries – across ambulatory care, hospital services, pharmacy, dental, vision, home health, skilled nursing, physical therapy, psychological counseling, and health education. The combined entity would serve almost 4 million members in 15 states with revenues exceeding $8.5 billion.

Consumer and physician groups urged state regulators to block it. The market concentration numbers were legitimately alarming:47 percent of the Medicare HMO market in Los Angeles County, 66 percent in Orange County, 70 percent in San Diego County. The California Medical Association opposed it on efficiency grounds, the evidence that large-company mergers produce meaningful savings was thin then and it’s still thin now. The FTC investigated. The state AG investigated. Neither acted. The merger closed in early 1997.

And Gumbiner, who had built this thing across 35 years, who had invented the Medicare risk contract, who had created clinical infrastructure across nine states when managed care was barely a concept, was out.

I’m writing this for ACO Watch, which means my readers understand the through-line I’m about to draw. So let me draw it directly.

The organizational model Gumbiner built, i.e., prepaid, prevention-focused, fully integrated, actuarially disciplined, with employed physicians and owned facilities, is what every serious accountable care framework since 2010 has been trying to reconstruct, imperfectly, at scale, inside a payment system that was never designed to support it. The MSSP. ACO REACH. The forthcoming LEAD Model. They are all, in their distinct ways, attempts to reimpose Gumbiner’s original logic onto a fee-for-service chassis that keeps metabolizing the intervention and returning to equilibrium, ergo the assimilation phenomenon.

The fundamental misalignment he identified, i.e., a payment system that rewards illness management over health maintenance, has not been solved. It has been managed around, at the margins, with shared savings arrangements that generate meaningful but modest results. MSSP produced a record $2.4 billion in savings in 2024, and that’s real. It’s also modest relative to total Medicare spend, and the structural incentive failure underneath it is still compounding.

What Gumbiner’s story adds to that conversation is a specific and underappreciated caution: governance matters as much as model design. FHP didn’t fail because prepaid group practice was wrong. It was absorbed (assimilated then corrupted) because the governance structure, i.e., the board composition, the shareholder dynamics, the CEO succession, drifted away from the founding logic without anyone being able to stop it. The mission got managed out of the mission-driven organization.

So as Sachin Jain recently opined, it’s about leadership. Nope! It’s the ‘OG&E’ (organization. governance and equity) foundation. Every ACO, every value-based care arrangement, every innovative primary care model operating inside a larger health system is subject to exactly this risk. The same board dynamics, the same quarterly earnings pressure, the same management consulting ‘Beltway Bandit‘ logic, i.e., B Cubed where bullshit baffles brilliance, almost reflexively says consolidation creates efficiency, yada, yada, yah. These are the forces that ended FHP, and they are operating today with considerably more sophistication and regrettably due to our healthcare ‘leaders‘ failure to lead, with considerably less resistance or pushback.

The Third Career, and What It Tells Us

There’s a postscript to the Gumbiner story that I find both moving and instructive.

After FHP was absorbed in 1997, Gumbiner turned to a project he’d been incubating since his first trip to Latin America in the early 1960s: the Museum of Latin American Art (MOLAA) in Long Beach, the only museum in the United States dedicated exclusively to modern and contemporary Latin American and Latino art. He purchased a former skating rink (a building type he apparently had a gift for repurposing), connected it to a former silent-movie studio, and spent more than $40 million over a decade building something remarkable. At his death in January 2009, he bequeathed over $50 million to MOLAA and the Robert Gumbiner Foundation.

He also funded the Ethnic Art Institute of Micronesia on the island of Yap. Of course he did.

Here’s what I take from the third career: Gumbiner was constitutionally a builder. He built 55 medical centers and four hospitals in nine states in his second career and then turned around and built a world-class art museum in his third. What he could not build, in the end, was an institutional structure durable enough to outlast the forces that came for it once the company went public and the governance shifted.

That is the cautionary lesson that belongs in every conversation about ACO governance, value-based model sustainability, and what happens to mission-driven organizations when they intersect with capital markets.

The dream was right. The architecture was real. The board got captured. And a $2.1 billion transaction later, it was over. Sound familiar (think the current dangerous to global and U.S> public health Charlatan at HHS and his unfit to lead minions at the commanding heights of our public health infrastructure.

The HMO, Taking It All Apart is available through Internet Archive and worth every hour it takes to read. Gumbiner earned the right to be bitter. He chose, instead, to be specific and to leave the record straight.

We should be paying attention.

==##==

** ** AI Use & Editorial Standards Disclosure. In producing this content, the author employed AI language tools in a defined supporting role: (1) Research aggregation: surfacing relevant source material and authoritative references across peer-reviewed, institutional, the arts and journalistic databases; (2) Structural organization: proposing content architecture and draft sequencing; (3) Draft suggestion: generating candidate language for author review. The author retains sole editorial responsibility for all published content. Every citation is independently confirmed as accurate and accessible prior to publication. No headlines, pull quotes, or factual claims are published without author verification. AI-generated language is treated as raw material then recast entirely in the author’s established voice and subject-matter expertise before any content reaches publication. This workflow reflects the author’s commitment to the standard that AI serve, not replace the author.

Part I: Leadership Isn’t the Problem. Leadership Is the Symptom.

By Gregg Anthony Masters, MPH**

Today I read a piece quoting the insights of Sachin H. Jain, MD, MBA, FACP, CEO of SCAN Group, SCAN Health Plan, and Forbes contributor, titled: “Healthcare’s problem isn’t the system, it’s us”.

The core argument:

The “it’s us“ indictment. In each of his three decades in healthcare, Jain has faced a different “boogeyman,” from the quality crisis to coverage expansion to today’s push toward value-based care. Each time, the industry implemented a fix, yet nothing improved. His conclusion: “It’s us. We’re not necessarily taking charge of the problems that are under our control.”

Toxic positivity as strategic evasion. Rather than acknowledging the real anger over cost, denials, and administrative burden, executives simply pointed to the flawed system. Jain’s view: “You can’t fix something until you actually acknowledge it’s a problem.” He concluded bluntly: “No one’s buying it anymore.”

The “no margin, no mission” trap. Jain cited a cardiologist at a Northeast academic medical center who built a heart failure program keeping patients out of the hospital. The hospital’s response was to ask what the department was doing wrong since admissions had dropped. When the physician explained the program was working, he was told: “No margin, no mission.” Jain argued this phrase has become a cover for exactly the kind of leadership failure he was describing.

Latent leadership capacity being killed. “We have so much more latent leadership capacity in this industry than we’re exercising. We have so many people with so much ingenuity, creativity, drive and passion, and we kill it.” His prescription: the number one way to improve healthcare is to tap leaders who genuinely support and desire an improved system.

Courageous challenge as organizational culture. At SCAN, Jain has made “courageous challenge” a core organizational value, giving employees explicit permission to stand up and say something that goes against the grain, creating an environment where difficult conversations and hard questions are not just tolerated but encouraged.

Accountability means being reachable. Every quarter, Jain sends his personal work email to each of SCAN’s 440,000 members and reads three types of messages daily: one from a satisfied member, one offering helpful advice, one who is angry. His view: “We hide behind HIPAA, we hide behind the ACA, we hide behind whatever rules we think we can hide behind.” vaticahealth

Depth over breadth, “monogamy” in provider-plan relationships. Jain argued healthcare is “extraordinarily promiscuous,” with providers partnering with every plan and plans partnering with every provider group. No one builds anything deep enough to change the patient experience. He pointed to SCAN’s strategy of asking provider partners to stop splitting membership across every plan and work with SCAN exclusively, asking what it would look like to have a shared call center, a shared patient record, and shared accountability for outcomes.

This ‘fireside chat’ triggered and prompted reflection on his argument and the need to reply via a series of posts to this audience.

Every generation of healthcare executives believes it has inherited a uniquely broken system.

It hasn’t.

American healthcare has been declared “unsustainable” almost continuously since Medicare and Medicaid were enacted in 1965. Costs have risen. Technology has advanced. Institutions have consolidated. Payment models have evolved from indemnity insurance to HMOs, PPOs, ACOs, bundled payments, Medicare Advantage, Direct Contracting, ACO REACH, and now artificial intelligence-enabled utilization management.

Yet one uncomfortable fact remains. The underlying economics have changed remarkably little.

That is why Sachin Jain’s recent essay, Healthcare’s Problem Isn’t the System – It’s Us, deserves attention. His central argument is provocative precisely because it rejects one of healthcare’s favorite excuses, i.e., that “the system” (aka the @HealthcareBorg) is somehow responsible for our collective inability to transform care and optimize outcomes.

He argues instead that healthcare’s greatest obstacle is leadership. Executives normalize dysfunction, defer difficult decisions, and hide behind complexity instead of exercising moral courage. It is a compelling critique because it contains more than a grain of truth.

Indeed, leadership matters. Organizations do not transform themselves. People do. But I would suggest Jain’s diagnosis stops one layer too soon:

Leadership is not the disease.

Leadership (or some may say absence of) is the symptom.

The disease is an incentive structure that rewards institutional preservation over institutional transformation.

That distinction matters because it explains why otherwise capable leaders repeatedly make decisions that appear timid, contradictory, or strategically incoherent.

We Don’t Have a Leadership Crisis

Contrary to popular opinion, American healthcare does not suffer from a shortage of intelligent executives. Quite the opposite.

Healthcare is populated by extraordinarily talented physicians, administrators, economists, data scientists, entrepreneurs, operators and yes, even actuaries. Few industries possess comparable intellectual capital.

Nor is there a shortage of strategic plans. Every health system now speaks fluent “value.” Every payer proclaims patient-centeredness. Every annual report celebrates innovation. Every conference keynote extols digital transformation. Every strategic retreat promises to “meet patients where they are.”

And yet fee-for-service continues to dominate organizational behavior. Not because executives secretly oppose value-based care. Because they are compensated to preserve existing revenue streams while cautiously experimenting around the edges.

That isn’t cowardice. It’s governance.

Boards hire CEOs to protect enterprise value.

Bond ratings.

Operating margins.

Market share.

Debt covenants.

Credit access.

Political relationships.

Employment stability.

The healthcare CEO who voluntarily cannibalizes profitable fee-for-service revenue in pursuit of uncertain long-term value may be admired by academics. Yet, he or she is far less likely to survive the next compensation committee meeting.

Leadership, in other words, operates within constraints that are rarely acknowledged in popular discussions about healthcare transformation.

Culture Doesn’t Create Incentives

Healthcare management literature frequently asserts that “culture eats strategy for breakfast.” The aphorism has become management orthodoxy. But in healthcare, incentives generally eat culture. Yet, truth is ‘culture’ follows payment. One need only observe how quickly provider behavior changes when reimbursement changes:

Hospital admissions.

Observation status.

Readmission penalties.

Risk coding.

Quality reporting.

Telehealth.

Hospital-at-home.

Every one of these evolved not because organizational culture suddenly matured but because financial incentives shifted.

Executives responded rationally.

As they should. This is not a moral failure. It is economics, full stop. Healthcare organizations are adaptive organisms. They evolve toward reimbursement, often quoting ‘no margin, no mission’.

The Myth of “The System“

Ironically, I agree with Jain on one point. Healthcare leaders often invoke “the system” as though it were weather. Immutable. Uncontrollable. An external force beyond human agency. But systems are not acts of nature. They are collections of incentives designed and continually redesigned by policymakers, regulators, employers, insurers, providers, investors, and consumers. The system behaves exactly as it has been designed to behave. Its outcomes may be undesirable. They are rarely accidental.

The ‘Missing’ Conversation

What remains surprisingly absent from contemporary healthcare leadership discussions is political economy, i.e., you can’t implement policy absent the enabling politics of ‘winning’ elections. Healthcare does not merely allocate clinical resources. It allocates financial power (minimally think proceduralist vs cognitive biases). Every reform proposal creates winners and losers. Every payment redesign redistributes income. Every consolidation shifts bargaining leverage. Every new benefit changes market share. Leadership, to the extent it can be ‘homogenized’ into best practices, alone cannot overcome those structural realities. Nor should we expect it to.

A Generation of ‘Deferred’ Decisions

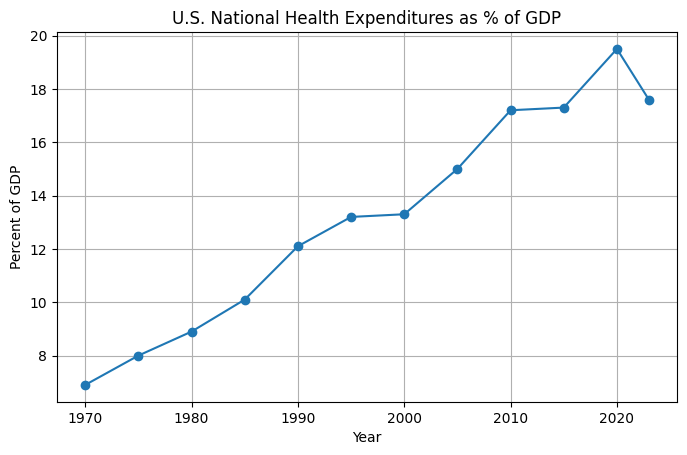

The irony is both persistent and painful. The healthcare industry has spent nearly forty years‘discussing’ transformation. When I started the GDP of healthcare share was 8-9 % range, today it’s just shy of 20%.

Secular themes, you know the organizing value proposition of push/pull industry top lines at major healthcare innovation conferences from HiMSS to HLTH with many in between including Health Datapalooza, JP Morgan Investor Healthcare Conference, NextMed (formerly Exponential Medicine and FutureMed, etc.) popularly engage:

Disease management.

Managed competition.

Integrated delivery.

Consumer-directed care.

Medical homes.

Population health.

Accountable Care Organizations.

Precision medicine.

Digital health.

Artificial intelligence.

Each promised structural change. Most produced incremental adaptation where one-off or niche (think Dave Chase and Rosetta innovation for self-funded employer sponsored health plans) vs. ‘systemic’ relief, i.e., advancing the triple let alone more ambitious ‘quadruple’ aim of clinician work/life satisfaction.

Why?

Because almost every reform was layered on a chassis of existing fee-for-service economics rather than replacing them. We reflexively create hybrid systems instead of new systems. Organizations therefore learned to optimize for both worlds simultaneously. Volume finances value. In turn value justified volume. Everyone learned the language and adopted the culture. Few changed the business model or associated incentive structure.

Where I Part Company with Sachin

This is where my conversation with Sachin begins rather than ends. He asks why leaders tolerate the status quo. I ask why boards reward them for doing so. He emphasizes courage. I emphasize incentives. He sees latent leadership. I see institutional equilibrium. Neither perspective is mutually exclusive. But one operates upstream from the other.

Coming Next

The debate over leadership inevitably leads to a larger historical question. How did American healthcare arrive here? Ironically, many of today’s strategic dilemmas were anticipated nearly forty years ago by one of managed care’s most consequential and controversial architects. Leonard D. Schaeffer believed healthcare organizations would eventually have to stop trying to partner with everyone. Instead, they would have to choose strategic allies capable of building scale together. Whether history vindicated that vision, or exposed its limits, is the subject of Part II.

==##==

Editor’s Note:

For Part II, I’ll trace Leonard Schaeffer’s move from HCFA to Blue Cross of California in 1986, the turnaround, the creation of WellPoint in the early 1990s, and the strategic logic behind selective payer-provider alignment, grounded in contemporaneous sources and Schaeffer’s own writings.

** AI Use & Editorial Standards Disclosure. In producing this content, the author employed AI language tools in a defined supporting role: (1) Research aggregation: surfacing relevant source material and authoritative references across peer-reviewed, institutional, the arts and journalistic databases; (2) Structural organization: proposing content architecture and draft sequencing; (3) Draft suggestion: generating candidate language for author review. The author retains sole editorial responsibility for all published content. Every citation is independently confirmed as accurate and accessible prior to publication. No headlines, pull quotes, or factual claims are published without author verification. AI-generated language is treated as raw material then recast entirely in the author’s established voice and subject-matter expertise before any content reaches publication. This workflow reflects the author’s commitment to the standard that AI serve, not replace the author.

by Gregg Anthony Masters, MPH & Fred Goldstein, MS **

PopHealth Week | Healthcare NOW RadioHost: Fred Goldstein, President, Accountable Health, LLC Executive Producer & Co-Host: Gregg Anthony Masters, MPH Episode Theme: “Enough Is Enough” – The Decimation of Public Health Infrastructure, the Rise of Health Quackery, and Why Science Still Matters

“Silence is acceptance people. Speak up!” – Gregg Anthony Masters, MPH, closing the episode

Introduction: When Professionals Say Enough

There comes a moment, sometimes quiet, sometimes explosive, when a person who has spent decades navigating institutions, absorbing dysfunction of ‘managing’ complex enterprises whether health plans or health systems, and advocating for incremental reform simply decides: no more. That moment arrived for Fred Goldstein, President of Accountable Health, LLC, and a recognized voice in population health, managed care, and evidence-based healthcare delivery.

On this episode of PopHealth Week, Fred once again stepped into the guest SME (subject matter expert) chair to unpack the essays he published on his PopHealth Pulse and LinkedIn under a title that said everything: “Enough is enough” and “People, Health, Research and Reality”.

His executive producer and co-host for the day, Gregg Anthony Masters, MPH, framed the conversation squarely and without ceremony: this was about the systematic dismantling of public health infrastructure, the ‘weapon-ization’ of social media against scientific literacy, and the long-unresolved contradiction at the heart of American healthcare – a system that was never really designed to produce health.

What followed was one of the most direct, experience-grounded conversations in the show’s run. No hedging. No false balance. Just two seasoned public health professionals, credentialed and candid, saying what the data and their careers have confirmed.

Part I: What “Public Health Infrastructure” Actually Means

One of Gregg’s most clarifying moves was to refuse the narrow definition of public healthinfrastructure and insist on the broader one. In popular discourse, “public health” often conjures health departments, ie, chronically underfunded agencies staffed by mission-driven clinicians who, as he put it, had to be “heart centered” to choose that career path “because the money ain’t there.”

But Fred and Gregg broadened the frame deliberately: legacy public health infrastructure (underfunded, often understaffed, overworked health departments, poorly synced with acute health care assets – think the ineffective handoff of Ebola cases in Dallas circa 2014) includes CMS, Medicare, Medicaid, and the full architecture of Title (XIX & XX) programs that fund and structure American healthcare delivery. It includes the research enterprise at NIH and the critical international disease surveillance network anchored by USAID. It includes housing policy, clean water, education, and the social determinants of health that account, by most estimates, for 80 percent or more of health outcomes.

This is not a rhetorical expansion. It is epidemiologically accurate. The World Health Organization defines social determinants of health (WHO) as the conditions in which people are born, grow, live, work, and age, coupled with decades of research confirm that income, housing stability, educational attainment, and neighborhood safety drive health outcomes more powerfully than any clinical intervention. When you defund housing programs, you are defunding health. When you eliminate food assistance, you are eliminating a health intervention. The infrastructure is one system, even if it is administered across dozens of agencies.

Fred named the pattern plainly: “what is being cut is not bureaucratic waste. It is the scaffolding that keeps people alive.”

Part II: DOGE, USAID, and the Epidemiological Consequences of Dismantling Global Surveillance

The conversation turned to one of the most consequential policy decisions in recent memory: the near-total dismantling of the United States Agency for International Development (USAID). Fred and Gregg cited this as one of the worst offenses in the broader campaign of senseless institutional destruction of modest public health interventions with a very high ‘return’ to the community.

USAID’s public health programs were not primarily charity. They were strategic. The agency maintained disease surveillance networks across dozens of countries, funded outbreak response capacity, and supported the kind of early-warning infrastructure that gives health systems time to respond before a pathogen becomes a pandemic. PEPFAR, administered through USAID, has saved an estimated 26 million lives since its 2003 launch. USAID’s tuberculosis programs treat millions annually in countries where, without treatment, extensively drug-resistant strains develop and spread – including, eventually, to the United States.

Fred stated the logic simply: we are interconnected. Pathogens do not respect borders or visa requirements. “Someone comes across on a cruise or a boat,” he said or, as the COVID-19 pandemic demonstrated, on a plane connecting through a major international hub. The current Ebola outbreak in the Democratic Republic of Congo was offered as a live example: the same kind of outbreak USAID was built to monitor and contain at the source.

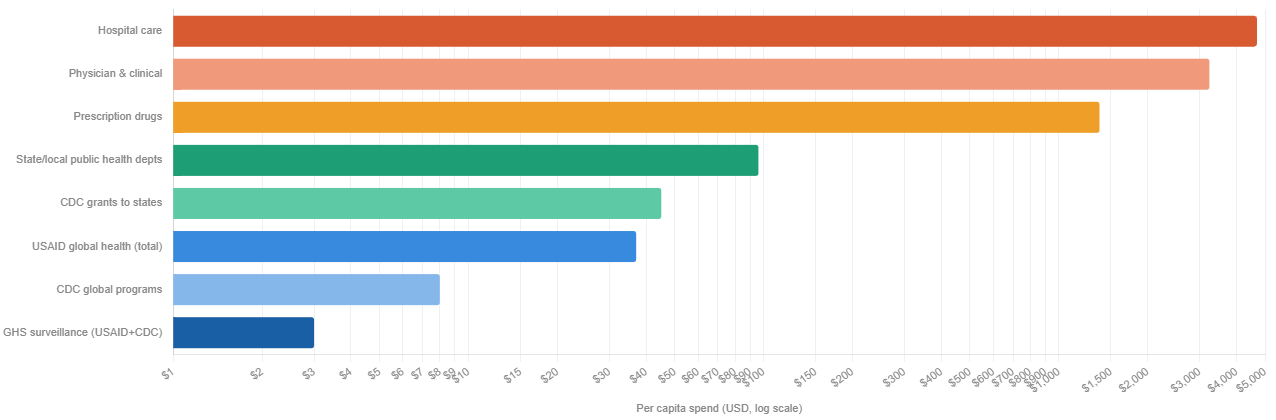

Investments in disease management vs. public health infrastructure

Ratio: hospital care vs. global surveillance 565:1

per dollar spent on global health security (GHS) programs

Public health as share of total spend

all prevention combined, per TFAH

COVID economic cost vs. 5-yr GHS spend

$14T loss vs. $1B prevention investment

Sources: CMS National Health Expenditure Accounts 2024; KFF; Trust for America’s Health; GAO; Johns Hopkins Center for Health Security. US population ~335M used for per capita calculations. CDC global programs ~$700M; GHS combined USAID+CDC ~$993M (FY2025 CR level). State/local public health includes federal grants to states.

The Centers for Disease Control’s Global Disease Detection program, which partnered closely with USAID, exists precisely because the cost of surveillance is a fraction of the cost of pandemic response. A 2019 report by the Johns Hopkins Bloomberg School of Public Health estimated that a severe respiratory pandemic could cost the global economy $570 billion annually. Defunding the early-warning systems that prevent such events is not fiscal prudence. It is a catastrophic risk transfer from the present to the future.

Part III: NIH Cuts and the Strategic Suicide of Defunding Research

Fred’s frustration was palpable when the conversation turned to NIH funding cuts. “The idea of cutting these NIH funds around research is just bonkers,” he said. “This country has been amazingly great and built upon the power of research.”

This is not nostalgia. It is economics. The National Institutes of Health funds research that has produced more pharmaceutical breakthroughs, more diagnostic innovations, and more clinical protocols than any comparable institution on earth. A United for Medical Research (UMR) 2026 Report: “NIH’s Role in Sustaining the U.S. Economy FY 2025” analysis found that every federal dollar invested in NIH research generates roughly $2.57 in economic activity. The mRNA technology underlying COVID-19 vaccines, developed with substantial NIH funding over decades, saved millions of lives and demonstrated that basic research investment has compounding returns that are impossible to predict in advance but catastrophic to forgo.

Fred invoked the HIV/AIDS research arc as the definitive case study in scientific iteration. From the first clinical descriptions of a mysterious immunodeficiency syndrome in 1981 to the identification of HIV, the development of AZT, the breakthrough of triple-combination antiretroviral therapy, the elucidation of viral load and CD4 counts as clinical markers, and the current era of PrEP, which can reduce the risk of getting HIV acquisition risk by as much as 99 percent in those who take it consistently – the arc took four decades of funded, iterative, sometimes-wrong-but-self-correcting science. None of it would have happened without sustained public investment.

“You never know what’s going to come out of some research project,” Fred noted. “It may lead to another great discovery.” This is not a platitude. It is the documented history of penicillin, of the polio vaccine, of chemotherapy, of statins. Defunding research does not eliminate need. It eliminates the capacity to meet it.

Part IV: The Scientific Literacy Crisis – How We Got Here and Why It Matters

Perhaps the most sobering section of the conversation addressed why false health claims spread so much faster than evidence. Fred and Gregg identified a convergence of forces:

1.Education gaps around scientific process. Most Americans never learn what science actually is, an iterative, self-correcting methodology that moves, as Gregg put it, “from unreasonable certainty to reasonable uncertainty.” Science does not produce Truth with a capital “T” on first contact. It produces provisional, probability-weighted conclusions that grow stronger with replication. That is not a weakness. That is the mechanism. But to someone who has never been taught how science works, the iterative nature looks like inconsistency, and inconsistency looks like unreliability.

2.Abbreviated attention spans. Fred cited an observation from a film school that younger students are struggling to sit through feature-length films because short-form social media content has restructured their attention patterns. The American Psychological Association (APA)has documented the relationship between heavy social media use and reduced capacity for sustained attention. Short-form claims, delivered with confidence, are cognitively easier to process than qualified, data-heavy arguments. Misinformation is almost always shorter than the truth.

3. The amplification of confident wrong voices. Fred described listening to a social media personality with millions of followers making claims he found “completely crazy.” His sons listened for ‘entertainment’. Millions listened for ‘guidance’. The Reuters Institute Digital News Report has consistently found that significant portions of the public receive health and science information through social media, often from sources with no relevant credentials.

4. The supplement and wellness industry’s exploitation of regulatory gaps. The Dietary Supplement Health and Education Act of 1994 created a framework in which supplement manufacturers bear no pre-market burden to demonstrate efficacy or safety. Claims that products “support” various functions proliferate without double-blind trials. Fred identified this as a deliberate exploitation of public scientific illiteracy and named it accurately as ‘health quackery’, given new life by a policy environment that values bold declarations over peer review.

Part V: The ADA Conference Incident – When Institutions Suppress Dissent

One of the episode’s most striking moments came when Fred described a scene at the American Diabetes Association’s recent scientific conference: researchers who had published an editorial in the ADA’s own journal, concerning NIH cuts and research funding, were handing out copies of that published work at the conference. They were escorted out by police!

This deserves to sit with you for a moment. A peer-reviewed article. In the associations own journal. Distributed at the association’s own conference. And the authors were removed by law enforcement.

Fred noted that subsequent resignations from the ADA followed. Gregg named the dynamic without euphemism: “there is a chill”. Professional associations that depend on relationships with federal funders, on conference sponsorships, and on not provoking regulatory scrutiny are making institutional calculations that silence their own members.

This is not unprecedented. Research on self-censorship in scientific communities has documented the ways in which funding dependencies, career pressures, and fear of political backlash suppress scientific speech, particularly on contested policy questions. What is notable is how openly it is now happening, and how quickly institutions that existed to advance scientific knowledge are retreating from that mission when it becomes inconvenient.

Part VI: The Broken Healthcare System: A Disease That Predates DOGE

Both Fred and Gregg were careful to separate two problems that are related but distinct:

Problem One: The current administration’s cuts to research, public health infrastructure, and social support programs. This is acute damage being done in real time.

Problem Two: The structural failure of the American healthcare delivery and financing system. This is chronic. It predates the current political moment by decades.

Gregg has tracked the evolution of this system with the granular attention of someone who has lived inside it. He walked through the arc: HMOs, then IPA spin-offs, followed by PPOs (which were more “palatable” to the group health market that didn’t want narrow networks), the ACA (Affordable Care Act) introduced ACOs, value-based care organizations, and corporate managed care organizations in various iterations. None of them, he noted, have solved the fundamental problem. They have created “more hurdles and obstacles for people to jump through to get needed care.”

Meanwhile: costs continue to accelerate driving widespread affordability claims as more and more of the liability shifts from plan to member via increased premiums, copays, coinsurance and deductibles due in large part due to the failure of House and Senate Republicans to extend ACA premium tax credits (subsidies). Meanwhile, access remains spotty. And quality is, in Gregg’s word, “a crapshoot.”

Gregg referenced a colleague’s new book “Healing the Sick Care System and Why Patients Matter” by Gil Bashe, which argues that the healthcare system views itself as the client, not patients. Fred agreed with the diagnosis but offered a defense of physicians: most clinicians entered medicine to help. The system does not allow them to. If a primary care physician in a fee-for-service environment keeps a patient healthy, that physician makes less money. A healthy patient generates no revenue. As Gregg further articulated: “There is no prevention business model as long as you run on a fee-for-service chassis.”

This is a structural incentive problem, not a character problem. And it is one that decades of health economics research has confirmed. Fee-for-service payment rewards volume and complexity. It penalizes efficiency and prevention. Value-based care models have attempted to reorient incentives, but Fred cited research suggesting the results have been modest at best – bending a 4 percent cost trend to 3.5 percent is not the systemic transformation advocates hoped for. The system, as he put it, “will not let” costs actually drop.

The brutal arithmetic of insurance: a health plan that successfully keeps its population healthy will collect premiums on a healthier pool, generate fewer claims, and in the ACA (Affordable Care Act) medical loss ratio framework find itself returning money if its loss ratio drops too low. The financial incentive structure does not reward health. It rewards the management of illness at a profitable margin.

Part VII: Physician Burnout as a System Failure, Not a Personal Failure

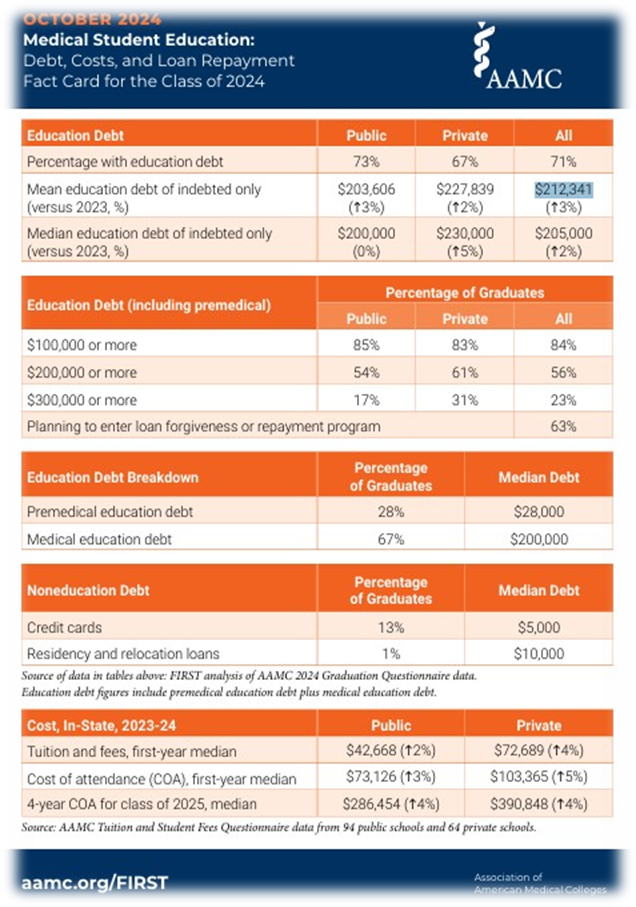

Gregg raised what he described as the ‘brain drain’ waste embedded in physician training coupled with growing exits to entrepreneurial or other administrative roles, ie, CMIOs. The public investment in producing a physician – four years of undergraduate education, four years of medical school, three to five years of residency, often additional fellowship training – represents up to a sixteen years of intensive investment, plus a debt load that for many physicians (public and private) averaged $212,341 according to Association of American Medical Colleges (AAMC) Medical Student Education: “Medical Student Education: Debt, Costs, and Loan Repayment Fact Card for the Class of 2024 “.

When those physicians burn out and exit clinical practice, opting for administrative roles, i.e., CMO (chief medical officer) and other positions, entrepreneurial ventures, or simply early retirement, the human capital loss is staggering.

The root cause is notindividual weakness. It is system design. Dr. Tait Shanafelt,professor of medicine and chief wellness officer at Stanford Medicine, describing the cultural mindset that long prevailed:

“There was this rite of passage mindset of: I went through it, it was formative – you should go through it too.”

Further, AMA research on physician burnout has documented the relationship between administrative burden, moral injury (being unable to provide care one knows is necessary), and the psychological costs of navigating prior authorization, documentation requirements, and corporate ownership pressures. When physicians are acquired by hospital systems or venture capital firms, clinical autonomy often diminishes. “They ain’t gonna let you do that,” Fred said, referring to the practice of prioritizing patient health over admissions and procedures.

The result is a primary care desert at precisely the moment primary care is most needed. Fred’s point was unambiguous: if you want to improve population health, you need more primary care access. You need more physicians oriented toward prevention, continuity, and the whole patient.

And ‘the system’ as currently designed actively discourages that.

==##==

** AI Use & Editorial Standards Disclosure. In producing this content, the authors employ AI language tools in a defined supporting role: (1) Research aggregation: surfacing relevant source material and authoritative references across peer-reviewed, institutional, the arts and journalistic databases; (2) Structural organization: proposing content architecture and draft sequencing; (3) Draft suggestion: generating candidate language for author review. The authors retain sole editorial responsibility for all published content. Every citation is independently confirmed as accurate and accessible prior to publication. No headlines, pull quotes, or factual claims are published without author verification. AI-generated language is treated as raw material then recast entirely in the authors’ established voices and subject-matter expertise before any content reaches publication. This workflow reflects the authors’ commitment to the standard that AI serve, not replace the author.

Healthcare leadership is rarely bold and too often ‘MIA’ when it comes the hard (risky) work of transforming our dysfunctional by design healthcare delivery and financing model about to implode on itself.

They’re generally risk averse and lazy bunch, preferring the hedge of ‘me too’ (what are my colleagues implementing?) strategies vs. the vision (and risk) of innovation’s upside potential when it comes to the transformational imperative to enable the triple aim (better care, superior outcomes at a lower per capita spend).

I’ve been in the ‘innovation space’ since the 80s in Southern California teaching doctors and hospital executives on the potential upside of managed care particularly as the model morphed away from closed loop systems (staff and group models) into a better fit with mainstream medicine, i.e, the IPA (Independent Practice Association).

Back in the day, HMOs were relegated to these limited and closed networks that primarily attracted 2nd and 3rd tier docs, often FMGs (foreign trained medical graduates) and the cohort within medicine that preferred the security of a salary at a staff or group model HMO vs. the entrepreneurial impulse to build a practice.

Amid current efforts to destroy vs. improve the ACA (Affordable Care Act) by defunding premium subsidies, here’s what we refuse to face, or that nobody wants to say out loud from the podium on social media, at networking parties or Congressional hearings:

With the advent of Maxicare’s ‘Window Project’ the penetration of mainstream medicine went full throttle to integrate HMOs into the growing pool of employer sponsored group health benefit plans, often side by side with ‘vote with your feet’ PPOs’. While also giving birth to the MSO (Management Services Organization) industry that provided essential infrastructure to assume and thrive under coordinated capitated payment terms.

The Lie We Keep Telling Ourselves

‘Medicare Advantage’ (MA) is NOT Medicare!

Let me translate: UnitedHealth coded harder, faster, and more aggressively than anyone else and got paid billions more because of it.

It’s not just a semantic quibble, nor splitting hairs per se. And it’s sure as hell not the technicality the MA lobby wants you to think it is.

Medicare Advantage is a term-limited contract with a private operator (MA plan) under Part C where CMS (the Centers for Medicare and Medicaid Services) ‘assigns’ the per member per year (PMPY) funds to the operator to administer Medicare-covered benefits under a capitation system. These terms and associated benefits are for one year. The operator can exit or change the contract terms, networks, formularies, utilization controls, and cost-sharing every single year. That’s not Medicare. That’s a commercial product wearing Medicare’s name tag.

As of January 12, 2026, the United States Senate just shoved that uncomfortable truth back into the national spotlight with a 105-page evisceration of UnitedHealth Group’s Medicare Advantage playbook.

Grassley Drops the Hammer: UnitedHealth and the Industrialization of ‘Diagnosis Capture’

Senator Chuck Grassley (R-Iowa), Chair of the Senate Judiciary Committee, released a majority staff report today that reads less like oversight and more like a forensic audit of a company that turned Medicare Advantage risk adjustment into its own profit-generating machine.

The thesis? UnitedHealth Group, the $400+ billion healthcare ‘too big to sail’ colossus that owns UnitedHealthcare, Optum, and effectively controls 10 million+ MA lives, has weaponized “diagnosis capture” including severity of illness/intensity of service upcoding at industrial scale.

In-home health risk assessments (HRAs) conducted by nurse practitioners whose job it is to find billable diagnoses

Secondary chart reviews by professional coders hunting for missed revenue opportunities

Pay-for-coding incentives to external clinicians – literally paying doctors to document more

Vertically integrated providers whose EHR workflows can be shaped by the parent company

AI-powered analytics identifying diagnosis opportunities where clinical thresholds are “squishy” (their word, not mine)

This isn’t a one-off compliance issue. This is the systemic architecture of a ‘healthcare borg’ that assimilates all material innovations intent on the transforming our paradigm from a fee-for-services, ‘do more to earn more’ model to one focused on the right patient, right care, right setting and time alchemy of a medical necessity driven model.

Grassley’s staff reviewed 50,000 pages of UnitedHealth documents including training materials, internal policies, software tools, audit protocols, etc., and concluded that UnitedHealth “turned risk adjustment into a major profit-centered strategy, which was not the original intent of the program.”

Industry publication Healthcare Dive reports that UnitedHealth “strategically captured a higher number of diagnoses and diagnosis codes than any other MA insurers – also resulting in higher CMS reimbursement than any of its peers.”

Now, UnitedHealth disputes the framing. They say their programs comply with CMS requirements and audits. Fine. But here’s the policy question that transcends any single actor:

Can a public program remain financially and clinically coherent when private plans are paid based on diagnoses, they are financially motivated to find?

OIG Already Told Us This – With Receipts!

If you want to know whether “diagnosis capture” is real, don’t read corporate press releases. Read watchdogs, including ACO Watch.

In October 2024, the HHS Office of Inspector General reported that diagnoses submitted only on HRAs and HRA-linked chart reviews, with no other service records tied to those diagnoses, drove an estimated $7.5 billion in MA risk-adjusted payments for 2023.

Read that again: Diagnoses that didn’t show up anywhere else in the encounter data still drove billions in payments.

STAT News’ coverage noted that UnitedHealth alone accounted for $3.7 billion of that $7.5 billion, almost half the total.

OIG’s point wasn’t “HRAs are always bad.” It was more damning: HRAs are vulnerable to misuse because they’re frequently administered by plans or vendors rather than a patient’s own treating clinicians.

The lack of any other follow-up visits, procedures, tests, or supplies for 1.7 million MA enrollees raises concerns that either:

The diagnoses are inaccurate (and thus the payments are improper), or

Enrollees didn’t receive needed care for serious conditions

Either way, taxpayers once again are the ‘bag holders’ for corporate greed..

MedPAC has been ringing the same alarm bells for years: MA risk scores remain higher than they would have been in traditional Medicare even after statutory adjustments, and coding intensity varies wildly across plans.

GAO documented years ago that coding differences can inflate risk scores and drive excess payments beyond what CMS adjustments have historically offset.

So, when a Senate report alleges a major payer optimized that vulnerability with uncommon scale and sophistication, it lands on pre-softened ground.

The Nursing Home Story: When Capitation Conflicts with Clinical Judgment

While Grassley’s report focuses on payment coding mechanics, there’s a second Senate track that’s even darker.

Senate Finance Committee leaders Ron Wyden (D-Ore.) and Elizabeth Warren (D-Mass.) have been investigating allegations related to UHG/Optum programs in nursing homes, specifically whether incentive structures designed to reduce hospital transfers create dangerous conflicts of interest.

A January 8, 2026 follow-up letter presses UHG for documents and details, citing heightened concerns and reported adverse outcomes, including at least three nursing home residents who allegedly died after being denied hospital transfers.

STAT reports that The Guardian’s December 2025 investigation spotlighted allegations that UnitedHealth’s cost-reduction programs may have resulted in deaths.

If the coding story is about who gets paid and why, the nursing home story is about something even more visceral:

What happens when the entity holding the capitation also influences whether a frail elder gets transferred to the hospital?

In managed care, “reducing unnecessary hospitalizations” can be good medicine. It can also be cost containment dressed up as care transformation. The line isn’t always bright which is exactly why Senate oversight matters here.

The Brand Problem: Stop Calling It “Medicare”

Now let’s talk about the part nobody wants to say out loud because it sounds too obvious:

If MA were truly “Medicare,” it wouldn’t need to borrow Medicare’s name to sell itself.

Yet the market reality remains: Consumers experience a daily blur of ads that imply they are “upgrading Medicare” rather than switching into a private plan with rules, restrictions, and networks.

So, here’s my position, plainly:

· MA is a private contract (Part C), not the Medicare program (Parts A & B under statute).

· Advertising should never use “Medicare” as a branding shortcut that obscures the private nature of the coverage.

· At minimum, any marketing that uses “Medicare” prominently should be required to state prominently, that it is a non-government plan option and not the Medicare program itself.

This is not anti-choice. It’s pro-informed consent.

The Selection Problem: Cherry-Picking Without the Cherry-Picking

MA plans are required to accept all applicants in their service area during appropriate enrollment periods, but “selection” doesn’t only happen through formal denial.

KFF’s analysis notes that people who enroll in MA spent $1,253 less per year in traditional Medicare before they switched, even after risk adjustment. That’s not MA making them healthier. That’s MA attracting healthier people. Let that sink in!

Research published in Health Affairs found that favorable selection into MA led to an average of $9.3 billion per year inoverpayments between 2017 and 2020.

KFF has also documented that people who disenroll from MA tend to have higher spending than similar beneficiaries who remain in traditional Medicare, consistent with risk dynamics and churn that can disadvantage higher-need individuals.

The Urban Institute’s comprehensive review concludes: “consistent and convincing evidence shows that favorable selection, after accounting for risk adjustment, is a key contributor to MA overpayment.“

When you combine favorable selection with coding intensity, you get a plausible recipe for a program that looks efficient while shifting financial pressure back onto the statutory Medicare program and taxpayers.

The Counterargument: MA Delivers ‘Value’ – Sometimes Real, Sometimes Theater

If we’re going to be credible, we must acknowledge what MA does offer:

An out-of-pocket maximum for Part A/B services (traditional Medicare does not have one unless paired with Medigap or other supplemental coverage)

Supplemental benefits (dental/vision/hearing and more) that many beneficiaries want and use

In many markets, lower premiumsand“bundle convenience,” including formulary (PBM) driven integration of Part D (the prescription drug plan)

Industry advocates also argue that some widely cited “overpayment” estimates are inflated by methodology and ignore program differences (like supplemental benefits and OOP – out of pocket- limits).

That’s the debate. But here’s the pivot:

Even if MA can deliver consumer value, it does not follow that “coding games” and “misleading branding” are acceptable collateral damage.

We can preserve consumer-facing benefits AND reform the incentives that distort coding, care, and communication.

What Reform Could Look Like (Without Blowing Up Choice)

Here’s a practical reform stack—built from watchdog findings and policy logic, not ideology:

1. Stop Paying for “HRA-Only” Diagnoses Without Corroboration

OIG’s findings make this the low-hanging fruit: If a diagnosis exists only in a plan-driven assessment and never appears in follow-up care or encounter records, it should not drive payment without additional evidence.

2. Strengthen RADV and Data Validation with Real Consequences

The MA payment engine runs on diagnosis data. Audits have to be scalable, timely, and consequential, or they become theater.

3. Align Risk Adjustment with Clinical Action, Not Just Documentation

If diagnosis capture is “real,” it should show up as care plans, monitoring, meds, referrals, or resource use. If it doesn’t, why is Medicare paying as if it does?

4. Truth-in-Advertising: Stop Calling MA “Medicare”

Make the distinction unavoidable in marketing:

“a Private plan option“

“Not the Medicare program”

“Plan networks and prior authorization may apply”

Plain-English trade-offs

5. Rebalance Incentives So Plans Win by Keeping People Well, Not by Finding Codes

Risk adjustment is necessary, but it shouldn’t be a profit center.

Bottom Line: The Medicare Brand Must Mean Something

The Senate’s scrutiny of UnitedHealthcare, paired with watchdog evidence on coding intensity, should be a wake-up call for policymakers, providers, and patients.

This is not a niche compliance squabble. It’s a structural integrity issue for a massive public-private hybrid that now covers tens of millions of older adults, including this author.

If you want to keep Medicare sustainable, you need two kinds of honesty:

Payment honesty (diagnoses should reflect reality and care), and

Marketing honesty (Medicare Advantage is not Medicare)

Because when a private contract markets itself as a public promise, and when diagnosis codes become a revenue stream, we don’t just risk overpayment.

We risk public trust.

And once that’s gone, good luck sailing anything – Medicare included.

==##==

** AI provided an assist via background research, organization and validation of claims as supported or challenged by authoritative 3rd parties, ie, academia, government, NGO or industry sponsored case studies.

Quick FAQ

Is Medicare Advantage the same as Medicare? No. Medicare Advantage (Part C) is offered by private insurers under contract with CMS; Original Medicare is the federal program (Parts A & B).

Why is MA under Senate scrutiny? Senate investigators are examining whether some MA practices—such as aggressive diagnosis capture for risk adjustment—may inflate payments, and whether certain care models create problematic incentives (e.g., nursing home hospital transfer decisions).

What is “risk adjustment” in MA? CMS pays plans more for members coded as sicker (higher risk scores) to discourage avoiding high-need patients—yet it creates incentives to maximize diagnoses.

Do MA plans have benefits Original Medicare doesn’t? Often yes—out-of-pocket limits for Part A/B services and supplemental benefits like dental/vision/hearing are common.

Gregg Masters, MPH, is a health policy analyst, public health and patient safety advocate and founder of ACOWatch.me. Follow him on social media @GreggMastersMPH or visit www.EndNMP.org or 2healthguru.wordpress.com for more analysis.

The news is monumental for the cannabis space and public health writ large. Here’s what actually happened today (Dec 18, 2025) and what the Trump cannabis Executive Order (EO) actually does – plus the 280E implications and the road ahead.

An interesting ‘sidebar‘ came via CMS Administrator Oz who indicated beginning Q2 2026 (April), CBD will be available for ‘free’ via physician order from ACOs, noting as well Medicare Advantage plans are ‘evaluating’ whether to include CBD in their supplemental benefits offerings to seniors as well.

We do live in interesting times!

Considering the relative underreporting of this signature event in the cannabis space, I’ve compiled a news summary and ‘explainer’ for your consideration with an AI assist in research and claim validation.

The news in plain English

President Trump signed an EO titled “Increasing Medical Marijuana and Cannabidiol Research” directing the Attorney General to complete the already-started federal rulemaking to move marijuana from Schedule I → Schedule III “in the most expeditious manner” (while staying within the Controlled Substances Act process). Source:The Washington Post+3The White House+3The White House+3

This is significant because it’s a White House-level push to break a procedural logjam: the Schedule III proposal has been pending since DOJ’s 2024 proposed rule and was sitting in the administrative hearing phase that got postponed. Source:Federal Register+2DEA+2

Directs the Attorney General to “take all necessary steps” to complete the Schedule III rescheduling rulemakingas fast as possible, consistent with 21 U.S.C. § 811 (the CSA scheduling process).

Directs White House legislative staff to work with Congress on updating the statutory definition around hemp-derived cannabinoid products (esp. “full-spectrum CBD”) and building a regulatory framework (e.g., THC-per-serving concepts).

Directs HHS/FDA/CMS/NIH to develop research methods/models using real-world evidence to improve evidence and standards of care around medical marijuana/CBD.

Includes standard language that it doesn’t create enforceable rights and must be implemented consistent with law/appropriations.

Important nuance: The EO is best read as an acceleration directive, not a magic wand that unilaterally “changes the schedule tomorrow.” The CSA still routes the change through the administrative rulemaking record. Source:The White House+2Federal Register+2

Does this eliminate 280E – and who benefits?

What 280E actually says

IRC § 280E disallows deductions/credits for businesses “trafficking in controlled substances”, “within the meaning of schedule I and II” of the CSA. This otherwise normal deduction of routine operating expenses has put cannabis dispensary operators (multi and single state) as a distinct competitive disadvantage. Source: Legal Information Institute

The key implication

So, if marijuana is finalized as Schedule III, 280E no longer applies to marijuana trafficking (because 280E is keyed to Schedule I or II, not III). Source: Legal Information Institute

Medical only, or recreational too?

Not medical-only. If marijuana is Schedule III federally, the 280E relief would generally benefit state-legal operators regardless of “medical vs adult-use” label, because 280E’s trigger is the schedule, not whether a state calls a sale medical or recreational. Source: Legal Information Institute

But: rescheduling does not federally legalize adult-use commerce; it just removes this specific tax penalty once the rule is final/effective. Source: The Washington Post+1

Timing: when would 280E relief actually start?

Not on EO day. It starts only after a final rule is issued and becomes effective (typically after Federal Register publication with an effective date). Until then, operators are still under the current Schedule I framework for federal tax purposes.

Why the EO matters (even though it’s “only” rescheduling)

If Schedule III is finalized, the high-impact wins are:

280E relief → ordinary business deductions return (rent, payroll, marketing, etc.), which can materially change cash flow and valuation math for operators. Source:Legal Information Institute+1

Research friction decreases vs Schedule I, potentially expanding clinical research and product development pathways. Source: The White House+1

It’s a federal acknowledgement of medical use, aligning more with current state realities—without ending federal control. Source: The White House+1

What it does not do

Even with Schedule III (and certainly with just the EO):

No federal legalization of recreational cannabis.

No interstate commerce greenlight for state markets.

No automatic SAFE/SAFER banking fix (banks still weigh federal illegality/risk; legislation is the clean solution).

No de-scheduling (removal from the CSA schedules entirely).

No broad criminal justice reform baked in (Editor’s note: some say the absence of AG Bondi at signing ceremony is a curious absence?).

(Those limits are why some coverage frames this as big-but-not-the-finish-line.) Source: AP News+1

What’s next (near-term roadmap)

DEA/DOJ completes the administrative process: resolving the stalled posture and moving to a final agency action. The rule has been pending since DOJ’s May 2024 proposed rule, and the hearing phase was postponed. Source: Federal Register+2DEA+2

Final rule published (Federal Register) + effective date.

Litigation risk / judicial review: major federal changes like this often draw court challenges, which can affect timing and certainty.

Parallel track: Congress (banking, taxation, states’ framework, descheduling bills) if political will exists.

Road to full de-scheduling (the real “endgame”)

De-scheduling generally requires Congressional action (amending the CSA) or a far more sweeping administrative move than the current Schedule III track – and it also runs into broader regulatory architecture questions (FDA framework, commerce, taxation, public safety, treaties). Practically, most paths to true normalization run through Congress.

Bottom-line?

The December 18, 2025 signing ceremony delivered a headline that – depending on where you sit – reads like long-overdue common sense, political triangulation, or a regulatory Rorschach test: President Donald J. Trump signed an executive order titled “Increasing Medical Marijuana and Cannabidiol Research.”Source:The White House

Here’s the crucial nuance right up front: the Executive Order (EO) does not itself reschedule marijuana. Under federal law, rescheduling happens through a formal rulemaking process anchored in the Controlled Substances Act (CSA) – not by presidential decree. What the EO does is direct the Attorney General to “take all necessary steps” to complete the ongoing rulemaking to move marijuana from Schedule I to Schedule III “in the most expeditious manner in accordance with Federal law,” explicitly referencing 21 U.S.C. § 811.Source:The White House+1

If you’re running a state-legal cannabis business – or tracking one from the investor side – the part that lands like a thunderclap is the tax angle:Schedule III would typically remove cannabis from the scope of IRS Code Section 280E, the federal provision that disallows ordinary business deductions for “trafficking” in Schedule I or II controlled substances. Source:Legal Information Institute+1

Let’s unpack what’s actually in the EO, why it matters, what it likely means for 280E (medical and adult-use), and what “next” looks like on the road to full de-scheduling.

What the Executive Order actually says (and does)

The EO frames federal cannabis policy as lagging behind widespread medical use and clinical reality—particularly around chronic pain, seniors, and veterans. It argues that Schedule I status has “impeded research” and left patients and clinicians without adequate guidance. Source:The White House

The operational heart of the order is Section 2, which sets out three main directives:

Expedite Schedule III rescheduling (Attorney General). The EO instructs the Attorney General to move the rescheduling rulemaking forward “in the most expeditious manner” under the CSA, citing 21 U.S.C. § 811 – the statute that governs adding, removing, or transferring substances between schedules through rulemaking and hearings. Source: The White House+1

Push a legislative/regulatory pathway for hemp-derived cannabinoids and full-spectrum CBD (White House Deputy Chief of Staff + Congress). The EO calls for working with Congress to update the statutory definition and establish a regulatory framework, including THC-per-serving limits and ratio considerations. Source: The White House+1

Accelerate research methods and “real-world evidence” (HHS, FDA, CMS, NIH). It directs federal health agencies to develop research methods—explicitly including real-world evidence—to inform standards of care and improve lawful access to hemp-derived cannabinoid products. Source: The White House+1

The EO also explicitly references the existing federal rescheduling process already in motion: DOJ issued a proposed rule in May 2024; the proposal drew nearly 43,000 public comments; and it is “awaiting an administrative law hearing.” Source: The White House+1

That matters because it signals the administration isn’t “starting a new process.” It’s trying to finish an already-started one – faster.

The rescheduling process is rulemaking on the record – no shortcuts