By Fred Goldstein, MS, Alexandria Skoufalos, EdD and Gregg Masters, MPH

Can you believe it’s been 20 years since the first Population Health Colloquium? Back then, we were just a few months into a new century. Maybe some of you even remember the concern over whether Y2K (a programming shortcut that used two digits to represent a year) would cause a worldwide crash of IT systems.

We’ve come so far in 20 years…and it’s been an amazing ride! As we gear up for this year’s Colloquium, we thought it might be fun to take a look back so we can understand how far we’ve come in the field of population health.

Let’s step into the Wayback Machine to 2001…

Population Health’s BIG bang coincided with the publication of Crossing the Quality Chasm. This milestone report turned the industry on its head by pointing out many of the delivery system’s flaws and problems with quality. The recommendations in this report created a roadmap to redesigning America’s healthcare system.

Fast forward to 2007 (year 6 of the Colloquium), when the Triple Aim was the main topic of conversation…and we’ve been talking about it ever since! That trend will continue until we finally get it right!

The Triple Aim used a 3-legged stool as a concept model in 2007 with Population Health as one of the 3 original legs.

Clinicians have been working hard to make things better, so much so that the industry added an unofficial 4th aim in 2014.

- Improving the health of populations overall

- Reducing the per capita costs of health care

- Improving the patient experience, and voila

- Improving the work life experience for clinical providers

Whether it’s the Triple Aim or the Quadruple Aim, is there a stool (or chair) here we can sit on?

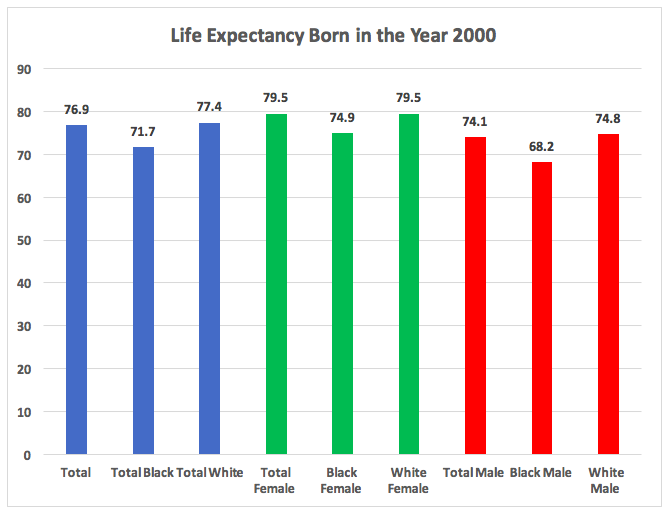

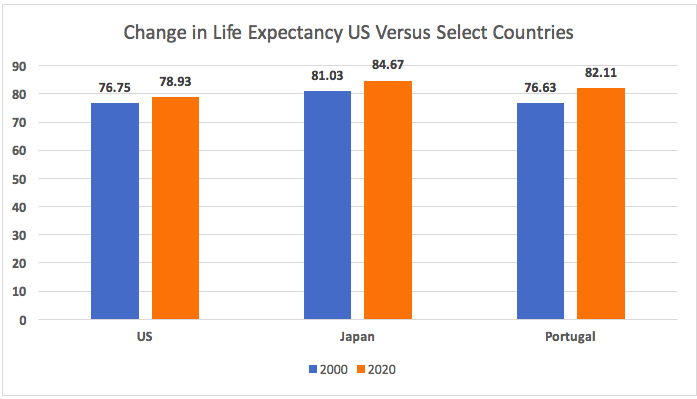

Let’s start with the first leg, Improving the health of populations. Life expectancy is a good measure of health.

According to the CDC’s National Center for Health Statistics, a child born in the US in 2000 had an  average projected lifespan of 76.7 years (74.1 for men and 79.5 for women). There are stark disparities in the range, though, if you drill down into the details (we’ll come back to that later):

average projected lifespan of 76.7 years (74.1 for men and 79.5 for women). There are stark disparities in the range, though, if you drill down into the details (we’ll come back to that later):

Although overall the North American continent enjoys the highest overall life expectancy, the US stats have not increased on par with other developed nations; in fact, they actually declined over some of the last few years.

During this 20 year period, the U.S. performed poorly, registering a modest increase of just 2.2 years overall. The rate of increase was affected by the fact that we actually experienced a reduction in Life Expectancy from 2014 through 2017 and a modest 0.1 increase in 2018 per a recent CDC report released January 30, 2020. During the same period, Japan showed a positive increase every year, and Portugal, which started slightly behind the US, showed a positive increase every year AND increased their Life Expectancy by almost 5 years,

During this 20 year period, the U.S. performed poorly, registering a modest increase of just 2.2 years overall. The rate of increase was affected by the fact that we actually experienced a reduction in Life Expectancy from 2014 through 2017 and a modest 0.1 increase in 2018 per a recent CDC report released January 30, 2020. During the same period, Japan showed a positive increase every year, and Portugal, which started slightly behind the US, showed a positive increase every year AND increased their Life Expectancy by almost 5 years,

https://population.un.org/wpp/Graphs/Probabilistic/EX/900

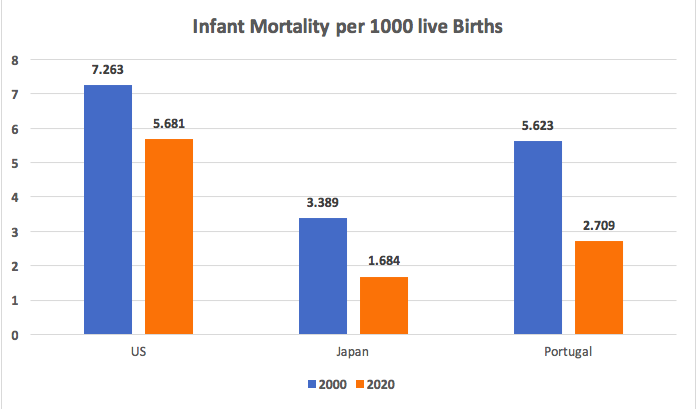

Infant Mortality is another good measure of population health. Let’s get a look at how we compare on that front with the same countries.

Infant Mortality is another good measure of population health. Let’s get a look at how we compare on that front with the same countries.

The US began the period with a higher infant mortality rate than either Japan or Portugal, and although we lowered our rates, so did they…and they outperformed us in terms of improvement, even though they began the period with lower mortality rates!

So as far as these measures and their association to improved health of populations, although we haven’t completely removed a leg, this stool is a little wobbly.

So as far as these measures and their association to improved health of populations, although we haven’t completely removed a leg, this stool is a little wobbly.

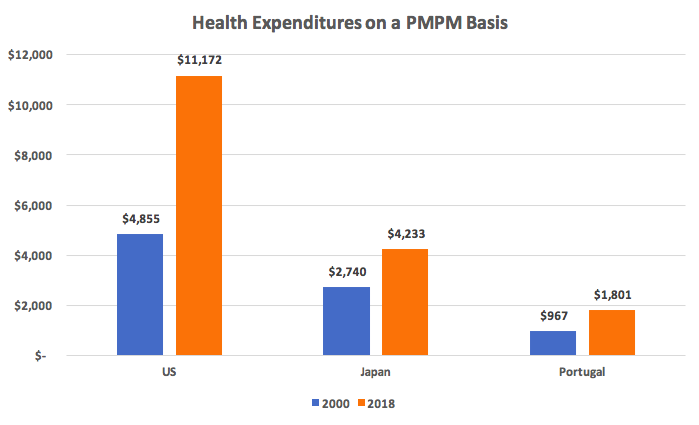

Let’s take a look at the next leg, reducing per capita costs.

“By 2000, health expenditures (in the U.S.) had reached about $1.4 trillion, and in 2018 the amount spent on health had more than doubled to $3.6 trillion. On a PMPM basis for the same time period the US increased 130% while Japan increased 55% and Portugal 86%.

(Source: KFF analysis of National Health Expenditure (NHE) data

This difference is well illustrated in the graph below on a Per Member Per Month Basis.

This leg of the stool has been practically sawn off!

One thing we in the US do better than anyone is spend money, and clearly this stool is in jeopardy of collapsing.

But, wait! We still have two more legs.

How about improving the experience of care?

Have you seen the headlines??

- Bankruptcies due to healthcare costs (even among those with insurance),

- Surprise bills

- Spiraling costs for pharmaceuticals

- Excessive wait times

- Access to data

The list goes on…and Americans are not pleased.

And what of the fourth aim, improving the work life experience for healthcare providers?

The burnout rate for clinical professionals is at an all-time high, with suicides showing signs of increase.

At a number of recent healthcare conferences, many people quote Bill Gates when discussing our future:

“We always overestimate the change that will occur in the next two years and underestimate the change that will occur in the next ten. Don’t let yourself be lulled into inaction.”

Bill might be correct in terms of computers, software, IT and Silicon Valley, but another axiom is “Past Performance is Indicative of Future Behavior.” Might this doom healthcare forever? Or, is this the year we stand up at this Colloquium, and say

“NO!

We have planted many seeds over the past 20 years; some have sprouted and are growing, others may be close to harvest! We can drive change by focusing like a laser on the Quadruple Aim as one stool with 4 equally important legs…because if it won’t stand, neither will we.

Make 2020 the year of transformative change. Join us at the Population Health Colloquium. We can’t afford to waste a single second!

==##==

:

: